Disclaimer: I work full-time for Hashed, who are active participants of the Terra blockchain and Anchor Protocol. This proposal is a result of constant discussions with the gigabrains at my workplace, supported by chats with active community members and the degens at GT Capital.

Context

Anchor is the heart of the Terra economy and will continue to be as Terra matures. Since Anchor’s launch in March 2021, TVL on the Terra blockchain grew from $540m to $12.6b – based on data from DefiLlama. A large part of it is attributed to Anchor’s dominance, either locked up as Deposits yielding interest or as Collateral being provided to take out UST loans.

Being a simple-to-use money markets protocol, Anchor has been instrumental in scaling UST adoption to the masses. A low-volatile stable 19-20% APY on deposits is an attractive marketing tool; as rightly shown with UST’s market cap growing exponentially from $1.2b at Anchor’s inception to $10.7b today. Moreover, many Dapps are built on top of Anchor – Astral, Kujira, Nexus, Pylon, Suberra, WhiteWhale, etc. – making it an essential building block of the Terra ecosystem.

In recent weeks, markets saw a downturn and an increasing number of users flocked towards stable yields (increasing deposits) and others borrowed less to avoid liquidations (reducing collateral staked and borrowing activity). This resulted in net negative cashflows and the yield reserve gradually depleting to maintain the deposit yield.

In Anchor’s current state, it may appear that its deposit yields are unsustainable. However, in the mid-long term, Anchor has future plans for vast improvement in its mechanics. This includes a new v2 borrow model to incentivise borrowing, onboarding of new POS assets as collateral, cross-chain deployment and changes in tokenomics. This refinement process takes time and we believe having a sufficient yield reserve to continue scaling UST’s growth to newcomers and inspire existing users’ confidence will benefit all stakeholders.

In this proposal, we projected the growth in Deposits, Collateral and Borrows over a 52-week period to arrive at a figure required for the yield reserve to maintain Anchor’s 19.3% APY. This serves as a buffer for the Anchor team to work on key protocol changes. The below segments detail the rationale behind the growth rates, which result in a proposal that recommends that the newly-created Luna Foundation Guard (“LFG”) contribute $450m to top-up the yield reserve.

Historical and expected future growth rates

Deposits

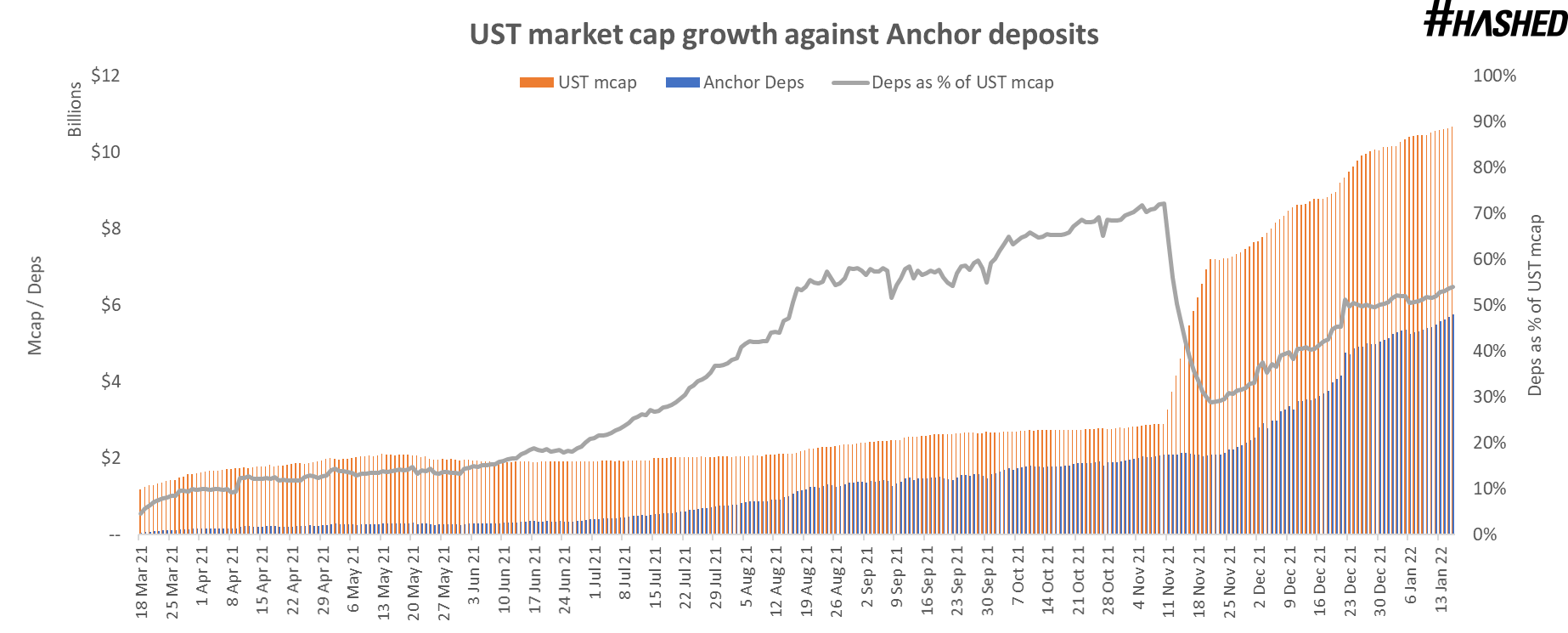

Anchor has seen 44 weeks of historical data, where deposits grew by a compound weekly growth rate (CWGR) of 11.4%. As Anchor grows in TVL, it is not expected that they grow at the same rate as before. Instead, growth should be a function of Anchor’s deposits as a % of total UST market cap.

Currently, Anchor has $5.8b in deposits against UST’s market cap of $10.7b – ratio of 54%. The grey line in the chart plots Anchor deposits as a % of UST’s market cap over the course of Anchor’s lifecycle. It is more realistic that as UST scales towards mass adoption, the proportion that flows into Anchor follows accordingly.

Since March 21, UST grew at a CWGR of 5.2% and Anchor’s deposits were on average 37% of UST’s market cap. However, this was weighed down by lower percentages in earlier months due to lack of awareness. The average ratio was 52.5% in the last 6 months (Aug 21 onwards) and we believe the forecasted figure will resemble that range.

In the base model, UST is expected to grow at 3.5% weekly and Anchor consumes 55% of UST market cap at any point in time.

Collateral

Collateral value had a historical CWGR of 9.3%, but a large part of that growth was due to the surge in LUNA’s and ETH’s prices. The more accurate approach to projecting collateral growth rates is to strip out the impact of the collateral’s price.

The actual amount of bLUNA grew by 5.3% weekly while bETH grew by 4.4% weekly. However, the growth of bLUNA has remained stagnant in recent months while bETH has shown gradual increases. With the rise of Terra dapps giving more use cases and differing yields for LUNA, it is expected that fewer users would want to sacrifice their LUNA as collateral for Anchor over time. The chart below shows the composition of both bAssets as a % of total collateral value.

One reason why bETH has not taken off as much as expected is because the steps required to move them to the terra chain & borrow UST and then move them back to Ethereum were too convoluted. As Anchor goes cross-chain, native lending and borrowing experiences should improve and the composition of collateral types should become more diversified across other bAssets.

Adopting assets like bSOL and bATOM would be significant drivers of collateral growth moving forward, resulting in bLUNA’s collateral dominance reduced to the 50-60% range. Cross-chain initiatives have already taken off, with Anchor’s collaboration with BENQI on Avalanche enabling sAVAX (liquid derivative of staked AVAX) to be used as collateral on Anchor’s v2.

The base model assumes a weekly growth rate of 3.6% and 3.5% for bLUNA and bETH respectively. The staking yield received on each bAsset is assumed to be 8% and 4.5% respectively – taken from data provided by SmartStake and Lido.fi. In the model, new bAssets are expected to be onboarded from week 12 onwards, with increasing proportions from 20%, 40% then 55% over the forecast period.

Borrows

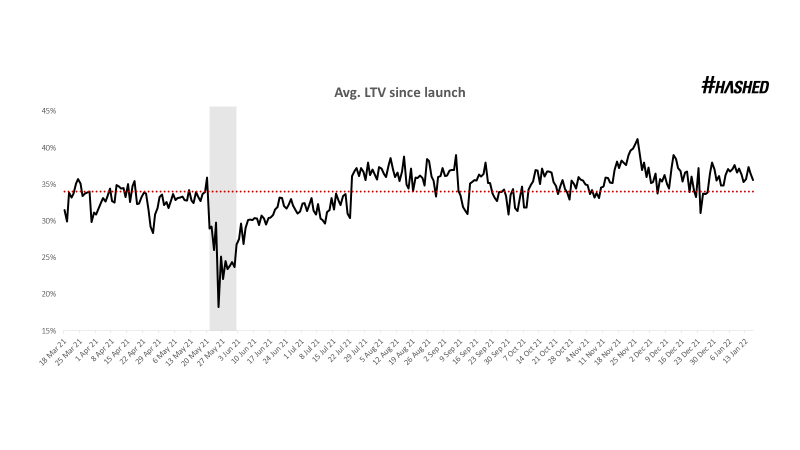

The interest collected from total borrowings is another key cashflow item for Anchor. Observing the LTV taken by users over time would be meaningful to projecting the future LTV. The red dotted line below shows that on average, LTV ratio was 34% over a period of 10 months; or 34.5% excluding the anomalies in the May 21 crash (shaded grey area).

The base model assumes an LTV of 34% and reduced interest multiplier at 0.2x.

Model assumptions & output

The assumed growth rates were plugged into a dynamic model forecasting cashflows received from (i) staking yield on collateral provided to Anchor and (ii) borrowing interest rates, vs. cashflows paid out to depositors.

The output were as follows:

In the base case, the yield reserve is only sustainable until Week 6 (that is, ~20 Feb at the time of writing). Thereafter, a top-up of c.$436m is required to keep Anchor functioning.

At the base case projected rates for deposits, collateral and borrows, Anchor continues to deplete the yield reserve even after the top-up at Week 6 – albeit at a decreasing rate of decline. This is until Week 47, where cash inflows finally grow more than outflows.

Self-sustainability may then be achieved, assuming the terminal growth rates hold.

Conclusion

Anchor is only 10 months old and has managed to record >$10b in TVL. This ranks the protocol as the second largest lending protocol on the blockchain, behind Aave which has been around for >4 years (previously known as ETHLend).

Topping up the yield reserve should be viewed akin to marketing expenses in bootstrapping an integral component of the Terra network. In fact, it might be the most effective way to scale UST to the masses.

Between the last time Anchor’s yield reserve received a $70m top-up to now, UST’s market cap grew from $1.9b (7 July 21) to $10.7b (current) – a staggering 5.5x increase, flipping DAI’s market cap to be the largest decentralised stablecoin on the market, and the 4th largest stablecoin in crypto. In that same timespan, Terra’s native token LUNA grew from a market cap of $2.7b to $21.4b (a 7.9x increase, though this may be attributed to multiple other factors).

If one were to measure the KPI based on mass adoption of that 70M Anchor ecosystem infusion, it certainly delivered healthy “returns” in a span of ~6 months. LFG’s goal mission is to support the Terra ecosystem and scale UST to make it the de-facto stablecoin in crypto, and Anchor is the best tool to achieve that – low-volatile yields on stablecoins might be the easiest and most attractive way to onboard the next 100 million users onto crypto.

The yield reserve top-up is a short-term solution to allow Anchor sufficient time for growth, with a v2 with improved $ANC tokenomics and mechanisms to incentivise borrows. In the long run, the goal is to ensure Anchor achieves mass adoption, yet is decentralised and self-sustainable. As a result, we recommend that LFG top-up the Anchor Yield Reserve with $450m.

LFG

LFG