Summary

Lower the tax rate to encourage higher on-chain volume.

Motivation

Historically, on-chain transaction volume on Terra Classic was the highest when 0 taxes were in effect (2.65b UST, 1/27/22) [1][2]. On-chain volume has decreased by -88.61% from the week prior: 198.02m LUNC to 22.56m LUNC. [3] By decreasing the tax rate, CEXs and other off-chain holders may be encouraged to return on-chain to enact trading, sustaining the cost for validators to run the chain.

Proposal

We are not burning nearly enough LUNC at the current tax rate. The tax rewards to-date since implementation of the 1.2% burn tax have totaled 3.67B LUNC [4]. While the relative rate of tax rewards generated from on-chain swaps are higher compared to historical levels when the Tobin and swap tax were implemented [5][6], the short-term gains come at a long-term cost, namely tax benefits in the short-term in exchange for economically unappealing on-chain volume projection for the long-term.

Validators can only sustain running the blockchain for so long before they become unprofitable to the point where they must shut down. If validators become collectively unprofitable, the blockchain shuts down without new ones taking their place. Any tokens that ‘live’ on-the-chain are not transactable without validators, meaning that users cannot cash out their holdings.

We do not have a full validator set as it is. In fact, the number of active validators has decreased from 90 to 83 in the last several weeks. [7] The ability for validators to issue LUNC rewards diminishes rapidly along with transaction volume, as validators create value by producing blocks, which are generated by transacting on the network. The new set will open near the end of October, but if we cannot make it until then, the tax’s negative effects may already have set in too deep.

The proposal is simple: we lower the burn tax rate from 1.2% to a significantly lower value as a compromise to encourage traders to come back on-chain. We begin by driving the tax down sharply as a way to encourage on-chain volume to occur. If this proves successful, we may reassess the efficacy of taxation on-chain depending on the ecosystem.

The values we use will correlate with the relative reduction in on-chain volume, or -88.61%. The new tax value is 0.2%, or more accurately, 0.16332% using the above raw data. Since we are using a sample of 7 days, and not the entire population of data, to calculate the proposed tax rate change, we must also factor in margins of error relative to our confidence levels before implementation.

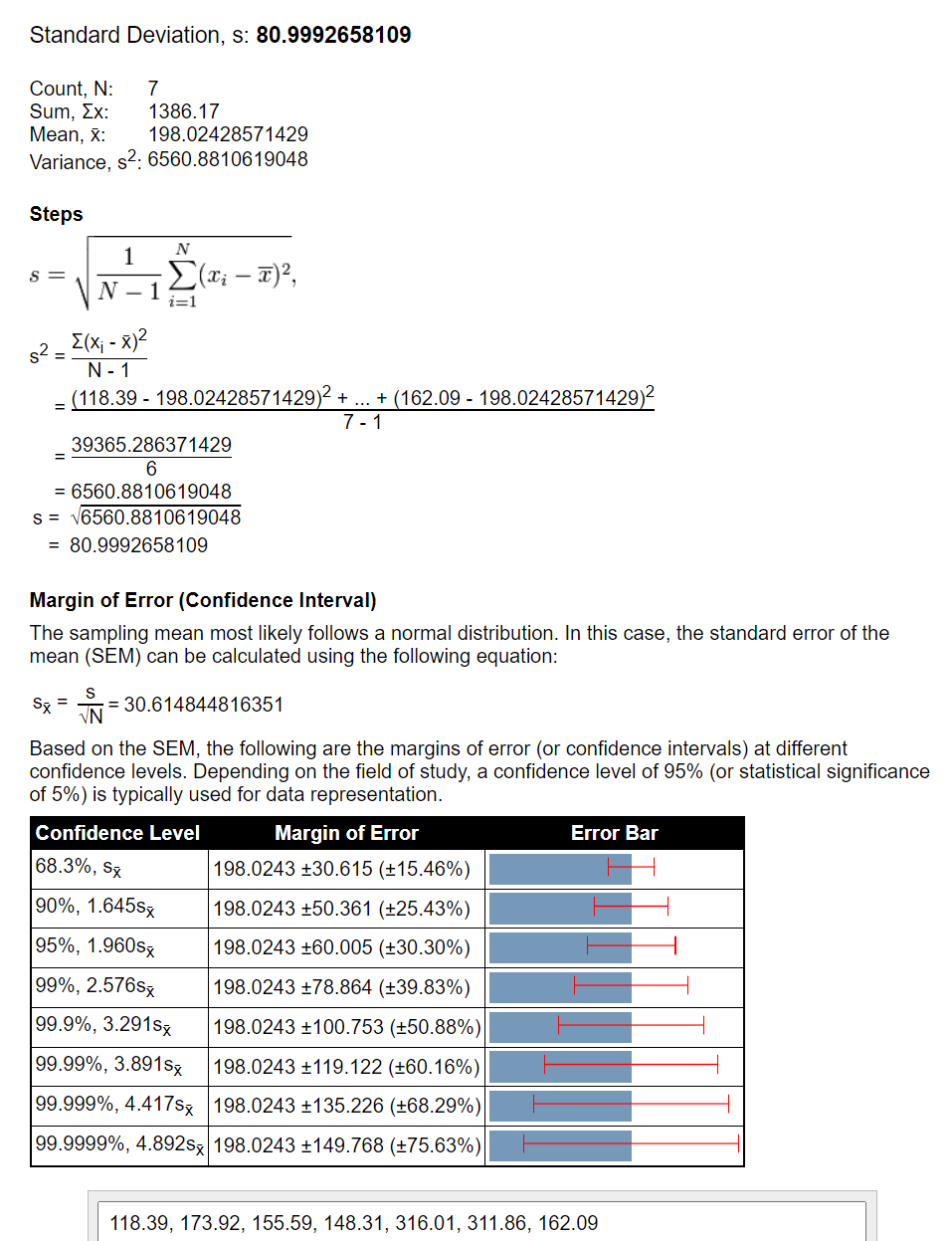

The first sample, or the trailing 7 days of tax since implementation, results in a standard deviation of ~9.548m LUNC transacted on-chain, with an average (mean) transaction value of ~22.562m LUNC. Our margin of error is ±31.35% at a Confidence Level of 95%. [8] In comparison, the 7 days of volume prior had a standard deviation of ~80.999m LUNC transacted on-chain, with an average (mean) transaction value of ~198.0243m LUNC transacted on-chain. Our margin of error is ±30.30% at a Confidence Level of 95%. [9] The difference in the margins of error is ±1.05%.

What we can take from this dataset is the relative bands which taxation rates on-chain affects the transaction values on-chain in a regression test. The sample sizes are small, but there are a variety of factors that affect transaction volume on-chain, such as availability of dApps to transact with (use). Therefore, we assume a higher confidence level with a greater margin of error in transaction volume, as it varies wildly. More importantly, we analyze the rate at which transaction volume pre- and post-tax deviates from one another, which is measured in the comparison of margins of error (±1.05% at ±30.30 - ±31.35%).

If we assume post-tax implementation margin of error is on the high end, we add an additional 7.073m LUNC transacted to our mean value, 22.5629m LUNC [8]. This value is 29.6359m LUNC transacted on “a better day.” On the other hand, pre-tax on-chain volume is measured at 198.0243m LUNC transacted on the mean, with a -30.30% deviation to the downside: a value of -60.005m LUNC transacted on-chain using this dataset, or 138.0193m LUNC transacted on “a worse day” - a difference of 108.3834m LUNC in potential transactions not performed on-chain. The important thing to note is how stark the margin of error is between comparable values. At a 95% confidence interval, and assuming tax is beneficial and no-tax is detrimental, the rate at which LUNC is being transacted on-chain is still 78.53% lower by having the tax in-effect on-chain. At the strongest levels of confidence in the samples of data (99.9999%), pre-tax transactional volume hits a low value of 48.2563m LUNC transacted against the mean value [9] and 40.2169m LUNC transacted post-tax implementation in favor of the mean value [8], meaning post-tax implementation has resulted in a decrease of transaction volume of -16.66% at the strongest confidence levels. The margins of error reach to values of ±75.63% - ±78.24% at these intervals due to the low sampling quantity. In short, the burn tax is pointedly punitive for on-chain transaction volume, which is a direct contributor to the desired effects of the burn tax (burning, or removing extra LUNC from the total supply). Instead of appealing to CEXs to adhere to this taxation in efforts to increase volume, we can compromise somewhere in between by lowering the lower tax rate. Tax Rates on Terra ranged historically from 0% to 0.35% + 0.50% (0.85%). We can alter the tax rate by proposing a change to the parameters mentioned in Proposal 3568 and distributed in Proposal 4159 (v22):

Changes

{

"subspace": "treasury",

"key": "TaxPolicy",

"value": "{\"rate_min\": \"0.0002\", \"rate_max\": \"0.0002\", \"cap\":{\"denom\": \"usdr\", \"amount\": \"60000000000000000\" }, \"change_rate_max\": \"0.0\"}"

}