Summary

The following is a proposal from 0rigin.one

I am not 0rigin, but I was given the green light to publish. You can find more about 0rigin (with a zero, not an O) by visiting their website at 0rigin.one

0rigin are some of the best economists I know in the industry. They do all of the economics for any projects I have ever worked with. They have high-profile histories in major banks and financial institutions. I will include the unformatted proposal and then upload the PDF right below here

Terra Luna Restructuring concept.pdf (1.3 MB)

Introduction

The collapse of Luna/UST relates to several factors from the macroeconomic environment, where

we have seen a general withdrawal of liquidity, and idiosyncratic flaws in the Luna model. Its not the

purpose of the paper to highlight mistakes but to establish some principles going forward so that

Luna/UST can focus on evolving into a rational functioning liquidity mechanism for decentralised

economies

The role of Luna/UST is analogous to that of a commercial bank and with the correct

implementation it should be able operate autonomously, gravitate to a truly decentralised

mechanism, and dynamically adjust risk parameters in rational fashion to optimise its solvency and

reward its stakeholders for their capital roles in the ecosystem.

Capital Structure

(1) We propose that the ultimate Luna/UST structure follow a classical Senior/ Subordinate

capital model

UST is now backed by LUNA as equity capital, with accumulated liquid assets as a senior capital

layer

This provides the model with a pool of assets that are now “Bail-in” capital but also can be utilised to

generate an asset return for the ecosystem which accrues to the Equity i.e. Luna.

(2) The primary economic driver of LUNA capital value is derived from the return on Non

Systemic Collateral (“Collateral”)

This Collateral can provide a yield or investment returns that are recycled into the Luna economy

but are unrelated to the economic activity or performance of UST.

This removes the recursive reliance on UST to provide LUNA’s capital value since it now has an

external independent economic relationship.

Earnings from UST can also be recycled to Luna holders but primarily these should be from market

activities such as lending spreads in the classical depositor/ lender set up.

All other things being equal, the value of Luna capital should grow exponentially with Collateral

since it receives direct returns on the asset bas,e as well as the catalytic benefits of a more stable

UST platform resulting from its backstop function for the asset.

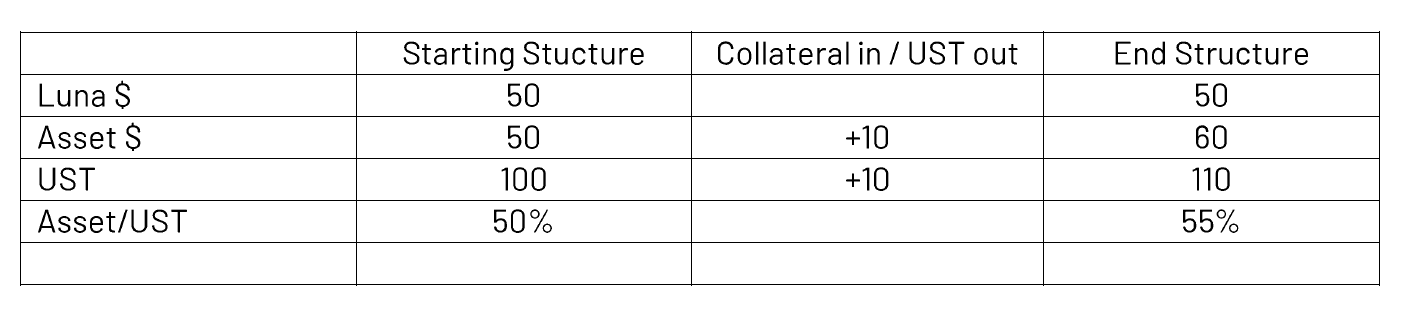

(3) UST should not be created from the burn of Luna. This was a key flaw in the model.

In our version of events, UST is created by the deposit of Collateral. A discounting

mechanism is implemented to reflect the asset swap and the consequent benefit to the

system which we visualise below in simple form:

We can see that assets sent in change the risk profile of UST from a 50% jump risk down to

45%. To maintain the same jump risk on UST, we could issue $20 of UST to the Collateral

provider for his S10 asset.

Since the risk profile has changed for all UST holders, and Collateral has increased for Luna

holders to generate returns on, it is simply a matter of allocating the benefit fairly between

the Collateral contributor and the protocol to calculate the fair discount on the UST issued.

A provider of Collateral is swapping in underwriting for the whole of the UST system which

then proportionately de-risks UST. It is comparable to writing puts and the discount on

UST issuance can be calculated on that basis. This can be modelled longer term using a

fairly standard derivatives model ( Merton et al.), incorporating a Kelley criterion/ sharp

ratio methodology essentially calculating and attributing risk/reward benefits between the

protocol and the Collateral (including riskiness of asset contribution).

At a high level, the discount for UST is proportional to the relative contribution of assets.

The same Collateral input will have a greater impact on the system solvency when system

assets are low and therefore the UST discount will naturally be larger at low solvency levels

to attract asset contributions. A calculus approach is also applied which smooths the rate

of change of risk for instance with large asset deposits.

The derivatives model also manages the fair value attribution when Collateral is greater

than UST issued (excess solvency).

This provides a rational pricing model for the contribution of exogenous assets.

It removes the capital preference that was granted to Luna holders previously, who were

able to take out a fixed USO obligation instantaneously to the disadvantage of those left

behind in the volatile asset.

( 4) The perpetual issuance of Luna to recapitalise UST holders needs to be reconstructed to

manage the hyperinflation (that can also be manipulated). Two rational measures that can

be implemented are:

(i) Dynamic Fixed Issuance

A fixed amount of excess primary Luna that can be issued that is determined

algorithmically by the solvency of the system. This still allows for large issuance as

equity approaches zero but contains the div#0 effect.

(ii) Bail-In Mechanism

Collateral swaps for Luna as UST price deteriorates. This should be based on the

system risk / solvency parameters. In simple terms, the collateral swaps to equity

to start absorbing losses as Luna price heads lower and issuance is approaching the

cap.

In addition we would propose that a new method is implemented that distributes Luna to UST

withrawals on an auction model for price discovery ( this also reduces oracle reliance). Such

auctions can incorporate a last-man standing approach to discount withdrawals on a curve that

relates to the proportion of withrawals. The benefits of the withdrawal discount are passed

back primarily to the existing UST holders.

This mechanism also avoids asset providers manipulating the asset pool to generate new UST

and burning immediately to create infinite amounts of Luna to effect ively take control of the

equity.

In (ii), we create an internal underwriting relationship between Collateral and Luna which

can be modelled ( paid for) using the amount of investment return or capital growth that is

used to pay Luna. More simply, a reserve is held for profits based around the riskiness and

solvency of the system for a bail-in of Luna.

In general, we do not susbscribe to limiting withdrawals or attempting to control markets as

these actions are antithetical to growth and scale

(5) The market price of UST should be accounted for in the mechanisms

(i) If the market price is below Sl. Collateral providers receive an amount of UST that is

greater than 1 :1, but less than 1/price: 1, together with new Luna (reflecting the

implied impairment).

This can be modelled from the system risk metrics in line with the overall

methodology and also incentivises more Collateral at lower solvency rates.

(ii) If the market price is above S1. we can invert the model in (i) sharing the benefits of

the arbitrage between capital providers and Luna holders.

Luna Risk and Economic Flows

Under this model, the equity nature of Luna is maintained but the recursive economics and

death spiral effects as a result of the prior model itself are removed. This allows Luna/UST

to now enjoy the outcomes on the true economic value of the Terra ecosystem.

Luna earns income from the Collateral capital which supports its own capital value

independent of UST.

We propose a Distribute/ Burn algorithm for the return distribution to Luna

of its revenue line. Included in this algorithm would be a component of UST

burning, which naturally benefits Luna holders.

The greater the Collateral, the higher the absolute returns attributable to

Luna (subject to normal market scale and capacity), the lower the direct risk

of loss, the greater the utility value of UST and the greater the catalytic

economic benefits back to Luna.

Luna earns income from the utility of UST as a financial instrument such as

lending and borrowing spreads ( in the style of a commercial bank).

This can be incorporated into the Distribute/Burn algorithm as above.

Luna circulation expands from impairment events in UST but contracts from asset

management revenue as well as demand for UST

Luna has protection from infinite issuance via a bail-in algorithm from Collateral

and a reserve/top-up mechanism.

This synthesises an equity rights issue (asset for equity swap) rather than

infinite quantitative easing and allows economic recovery for existing

stakeholders rather than a complete wipe out.

Asset holders are incentivised to collateralise the system to generate UST at

discounts that reflect their economic contribution but the model does not allow

them to arbitrage Luna holders.

The model is now rational and fair to its stakeholders in terms of risk and return on capital.

Further features

(1) Single Staking of Luna

This can be utilised to calculate the Distribute or Burn mechanics where Burn has a

relationship with (1-Staking). Essentially, when there is zero staking all revenue is burnt and

this reduces as staking increases.

Staked Luna can have governance rights which are used to white list assets tor the Non

Systemic Collateral pool and so on.

UST Staking and general yield

In any network economy there is a utility of the core currency. There is an equilibrium

liquidity requirement that is normally solved by the market. This liquidity produces

economic output and the market finds the equilibrium spot tor its actual requirements.

In UST we would want to encourage holders who are not using UST to deposit them back

into to protocol. This optimises utility for liquid UST but also reduces immediate withdrawal

risk on Luna and Collateral.

We would propose a staking model whereby UST can be staked across a time curve for up to

10 years( mirroring the standard bond markets).

An inflation rate is determined from:

(i) Duration weighted staking.

long term staking would have a compression effect on the inflation rate vs the same

amount of short term staking.

(ii) Market price of UST

Inflation rate paid in combination of UST and Luna depending on premium ( more

UST) or discount (more Luna)

Inflation rewards are locked up for the same staking period. We allow unlocking subject to a

haircut on assets based on the present value determined from the current inflation rate.

This allows rational liquidity to come back to the market i.e. if the economic benefit of

liquidity is> than the illiquidity yield.

The underlying inflation curve can be built from risk factors in the model since UST stakers

are deferring their rights to exercise a form of put option on the protocol. Again we share

the theoretical benefits.

(2) Decentralised Asset Management

Future implementation of a smart contract optimiser, with global risk parameters managed

through governance, to remove dependency on individuals or centralised entities.

(3) Immediate Actions whilst a model and road map is determined

Utilise an approximate discounting model to start building collateral backed UST following

the incentive dynamics ( more collateral lower discounting).

Remove the ability for Luna to burn into UST. This is the key problem that destabilises the

system.

Conclusion

This is a very preliminary assessment due to the nature of the situation at hand. However,

the principles herein are able to manage the current distressed capital structure, provide

a strong equity story for the Luna token and provide a model that will deliver rational

economics to the Luna holders.