Proposal Link on TerraStation → (Terra Station)

Summary

We are the team behind 2 other CMC 500 projects and happen to believe our strength is in the field of economics. We’ve monitored the event unfold and recorded numerous metrics that showcase the problem that caused the spiral downfall. I myself have experience with economic architecture and algorithmic trading.

This is a proposal for Economic restructuring, which shouldn’t be too difficult from a technical standpoint. We as members of the crypto industry wish to see UST and Luna back on their feet as it affects everyone. The industry would be better off if the project is saved.

The proposal is joint work by our team and we hope that the Terra community will look into it. It is based on extensive data and analysis.

Motivation

We are confident that LUNA and UST can be saved if specific actions are undertaken quickly. So far, the actions taken have only exacerbated the problem, as they happened to aim for a palliative solution and didn’t really treat the actual core problem.

In fact, they were exactly in the opposite direction of what was needed to be done and only worsened the situation.

Proposal

Before starting, we want to emphasize where the current problem is.

UST’s market cap represents a collective investment by all people who believe in the system of Luna.

In simple terms, a market cap is: x * y = k

x = supply

y = price

k = economic value

Since UST’s market cap is collateralized by Luna’s market cap, this means that the peg is valid only to the extent where (k)Luna doesn’t go below (k)UST.

We can assume, therefore, that

UST = liability

Luna = asset

And if the liability is greater than the asset, then a deficit arises and subsequent risk of default occurs

The algorithmic nature of the UST mint/burn fails to address the risk of external factors affecting the “k” factor of LUNA and there need to be critical mechanisms that protect and counter the incursion of such a deficit with strong pro-active mechanisms for monitoring and countering even the slightest probability for such a deficit.

A collapse in LUNA deems UST uncollateralized and an inversion takes place.

Generally speaking, k(Luna) / k(UST) needs to always come to 1 or more than 1.

Upon serious stress, a strong inversion may cause UST’s fair price to go below 1 which is also furthermore not acknowledged.

For instance if the market cap of UST is $10B and LUNA is $5B, then the “fair” price of the current version of UST would be $0.5. However, due to the psychological perception of UST being a stablecoin investors as well as arbitrageurs are artificially sustaining UST in a severely overpriced state.

For instance, at the time of writing this post, the price of UST is $0.441 and the price of LUNA is

UST market cap = $5000M

Luna market cap = $200M

UST fair price =0.04

UST actual price = 0.44

UST being overpriced by a factor of 11x

Why does this matter?

The rate of minting relies on an adequate fair collateralized rate of UST. With current settings, UST is by design predisposed to lose peg in times of crisis, and the design should be planned accordingly.

Instead of hoping for it to never happen, the system should be built with conscious awareness that it will happen and have the proper mechanics on how to deal with it. Similar to what liquidation events take place with lending. If played out properly, the liquidation itself also can play a key role in the long-term strengthening of the underlying protocol. In a similar way, an upeg can be managed, communicated with affected persons, and reacted to properly.

If the rate of minting accelerates, then it acts as a gravitational pull that exerts disproportionate pressure on LUNA in the opposite direction of where it should go.

Think of what an event horizon represents for a black hole. As an object gets closer to the event horizon of the black hole, the gravitational pull becomes stronger and stronger and there’s a point beyond which there’s no return.

In this case, Luna is the object that is being pulled faster and faster spiraling out of control into an infinite minting state. The good news is there may be a way to fix this.

And as UST price is artificially kept higher, it acts as an accelerator for LUNA’s downfall.

Our team has been logging the change of this multiplier and was able to verify that the current design is predisposed to such an “event horizon” tipping point vulnerability.

Important consideration 1:

Following the x * y = k formula for market cap, LUNA is affecting x by minting new supply, which doesn’t mean it is outputting new economic value. Instead, the uncontrollable minting state, put it as an extremely hostile stance towards new investors, because any potential investment gets diluted extremely fast.

Inflating the supply, just pulls more capital from investors towards the UST absorption mechanism, but doesn’t affect the economic worth of “k” which comes as a manifestation of investors’ trust and the ultimate collateral for that widely discussed absorption.

Important consideration 2: A stablecoin has one main priority: stability above anything else. Since an algorithmic coin is essentially a liability to the underlying asset, careful moderation on the relative size of the minted amount needs to be put in place at all times.

For instance, would you rather run a business with a 20% debt to asset ratio or a 100% debt to asset ratio?

And in times of market contraction, which one of the two would be more vulnerable?

The answer is unequivocal. By allowing UST to have been minted uncontrollably, the economy of UST/LUNA was technically allowed to run at 100% debt to asset with significant exposure to any corrections. As a comparison, all lending protocols (Compound, AAVE, and even tradiFi) trigger liquidation when 100% debt to base is reached (a.k. Loan-to-value ratio).

During a bull market trend, LUNA will naturally outgrow the market cap of UST, but during a bear trend, a contraction takes place at an even faster rate afterward. Based on this assumption, the maximum allowed debt to base of k(UST):k(LUNA) for minting of new UST to be allowed should be comfortably below the rate of the ratio that may be established in a bear trend.

Technically speaking you don’t need an enormous market cap for a stablecoin to serve its purpose as arbitrageurs naturally enable liquidity without the need for minting. And the lower a supply is on a stablecoin, the higher its utilization rate becomes.

And the higher the utilization rate, the stronger the organic arbitrage economy is which can dampen market shocks much more efficiently as they create zero exposure for the issuer.

Why things went really wrong:

Mistake Number 1)

Investing BTC reserves to support UST

Why it’s wrong: As outlined above UST is technically a liability and also to some degree a derivative of LUNA. You can twist the fabric of reality, but you can’t alter its course and in the same sense, spending BTC on boosting UST in times of crisis is equivalent to boosting liability. By boosting UST value, and LUNA being left out of control, the inverted multiplier of rate of minting is exacerbated that is at the root of the problem. UST’s rate being held artificially higher magnifies the inflation factor and boosts dilution without creating a new economic influx.

The outcome is a net negative flow of the economy as investors flee Luna in fear that they will be diluted even faster.

And again, similar to how an object has a point of no return beyond crossing an “event horizon”, this inversion causes Luna to accelerate more and more towards total loss.

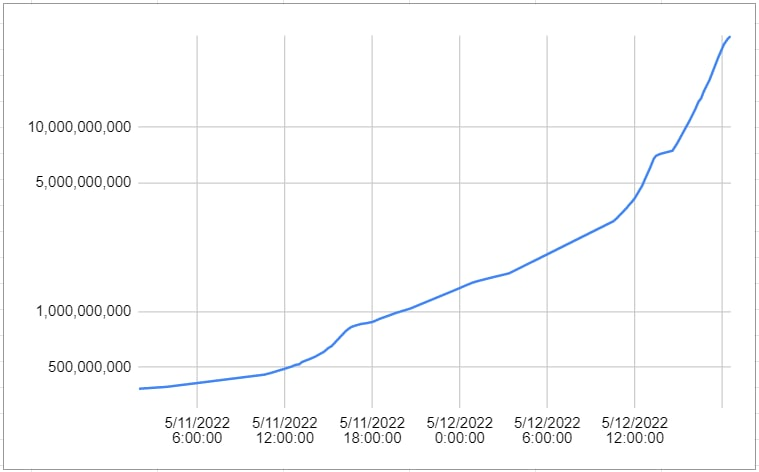

As it can be seen on this chart, the rate of growth is exponential with the drop of value becoming worst and worst.

Mistake Number 2)

Focusing on Increase of inflation → The proposed increase of mint capacity is nothing more than an even more aggressive dilution of investors which is in the exact same trajectory as mistake 1.

Mistake Number 3)

“Save UST - Forget LUNA” policy

Again it shows the strategy for mitigation. Without Luna there would be no UST and UST is just an extension of Luna.

Based on the above assumptions we can derive that:

-

UST is irrelevant if Luna is on a bad path. There’s no way to save a derivative instrument if the underlying asset goes to 0

-

Luna’s aggressive minting acts as a negative marketing factor to the community and investors and hurts the project more than it helps especially in times of crisis.

-

Minting alone doesn’t create new economic value (k), instead if sucks up whatever existing value there is from investors, therefore it needs to be handled with extreme care.

-

The accelerated inversion has an “event horizon” type of tipping point, which when Luna passes, enters into a black hole-like experience. With subsequent full collateralization of UST being possible only in an event of “singularity” between the two where they are compressed to a very small state (UST going down to near zero and LUNA going down to near zero would make UST collaterized again).

In theory, a reversal is possible, but highly improbable due to the continuous minting that scares off investors.

As we continue onward analyzing the change of the multiplier, there was a moment of light that took place when the entire chain was halted.

As you can see, the multiplier was reduced due to the Terra chain simply stopping work. This stop of minting caused a reaction in price on exchanges.

At that moment UST market rate decreased to one which was closer to the fair price, and Luna mint was halted.

Proposed Solution

On a high level:

The problem needs to be addressed in three layers. Luna, UST, and Anchor in order to make a more sustainable system without sacrificing the appeal.

Luna being the one with the highest priority, as it is the base for all others with an immediate focus on saving it first and rewarding, instead of hurting, the people that will decide to risk capital to support it.

Luna needs to cool-off. Minting is to be paused and the mint multiplier needs to go negative as soon as possible in order to raise investor confidence.

The money velocity should be significantly reduced in conjunction with minting, while the focus should be on utilization, redundancy mechanisms, and deflationary tools to stimulate demand for Luna beyond the UST minting.

Unfortunately, this will lead to UST market cap and price reduction in the short term, but it’s not necessarily a permanent one. The UST:LUNA relationship also resembles one of a liquidity pool, and UST can compress similar to what impermanent loss is to LP, as long as it is not redeemed at the low rate.

The market cap of UST can be compressed naturally, and allow breathing space for Luna to improve the probability of reversal.

After confidence in LUNA is improved, then it may be possible to decompress the market cap of UST back to the previous $1 peg. UST investors will have much higher confidence if they know there is a clear path of improving LUNA collateralization of their assets and not just random acts of artificial and short-term price support.

During the compression, Anchor rewards may continue to accrue but withdrawals to be disabled temporarily.

Specific proposed measures

1) Immediately halt new minting OR block producing and lockup all Anchor withdrawals for a period of 14 days (Deposits allowed). Halting new block production will prevent the system from further hurting its own self until it is patched and will also stop redeeming of UST for a short period of time, which will enable it to start compressing to its actual fair price.

2) Enable tiers on Anchor and bind the Anchor earn economy with Luna demand

- 6% for random people → Direct UST deposit

- 10% for bLuna owners $1k min → Deposit to lockup UST + bLuna

- 12% for bLuna owners $10k min → Deposit to lockup UST + bLuna

- 17% for bLuna worth $100k + lockup of 90 days → Deposit to lockup UST + bLuna (thus creating demand for both assets)

- Disaster buyback fund → Announce target plan to reduce circulating supply back to previous levels by enabling a buyback mechanism (Raise external fund with partners and institutions and use that as a separate economic pool to buy back and burn LUNA at a constant rate). With just $1B, and Luna price of $0.003 a staggering 333B LUNA can be bought back. This will not only have a fundamental play on the economy but also an enormous confidence-booster to investors.

The buyback can be executed in tranches and over a period of 6 months with 166M per month. This will also make it easier to secure the funds.

4) Enable a cap on the rate of newly minted UST, to increase the general utilization rate and strengthen the organic arbitrage economy with an additional decrease in money velocity. UST as a high interest-bearing asset needs to have limits and a sense of exclusivity. The initial proposal is to limit to no more than 10% to 20% UST supply increase per year and to have an additional limit to no more than 35% of the market cap size of LUNA. This would add a near 3:1 overcollaterization factor that will significantly reduce the probability of UST losing peg even in harsh market conditions.

In fact, if we break-down existing stablecoins according to Market cap/Utilization rate:

USDT Market cap 76B, Volume 50B → 78% utilization rate

BUSD Market Cap 16B, Volume 12B → 75% utilziation

USDC Market Cap 51B, Volume 7.8B → 15.3% Utilization

DAI Market Cap 6B, Volume 0.63B → 10.5% Utilization

UST Market Cap (prior to crash) 17B, Volume 0.6B → 3.5% Utilization

As it can be seen UST had a significantly underperforming utilization rate and minting new coins was not really necessary. Instead, a limit on supply should have been put in place in order to add a natural reserve to absorb market contraction.

Even with an applied cap on UST minting, Anchor’s model would still likely be capable to generate significant demand if tiered approach as described in step 2) was applied, because bLuna would be introduced as a prerequisite for the eligibility to benefit from the high APR product. Thus increase of utilization on UST without increase on UST market cap, would automatically imply an increase in demand for more people to enter into Anchor and lockup more bLuna. A feature that may offset the reduced demand factor from the more conservative setting on new UST minting.

5) Strengthen Luna’s economy around stability and staking and focus on a deflationary mechanism. Deflationary tools could be introduced to cut LUNA supply while not modifying the existing mechanics in place.

6) Put the CAP of UST at 20B UST, which could be changed only with a governance vote with a very high quorum. The cap will enable a deflationary nature of UST and facilitate stronger demand for it on a psychological level.

7) Enable a dynamic price oracle to monitor the ratios of k(LUNA):k(UST) and when collaterization falls below 1, affect UST price to controllably start compressing. This will avoid putting inverted pressure on LUNA. In conjunction with that, enable 80% (could be variable) of UST inflow capital to automatically go to a collaterized insurance fund that wll support LUNA and not UST.

The $1 peg is a hardcoded setting based on assumption that there’s sufficient collateral at all times.

Changing the peg temporarily to a lower impermanent price would not alter the way the current system works.

Yes, it will add stress to the investors, but on the other hand, when investors know that this is expected (yet less probable scenario), they may be incentivized to buy more UST at the lower price, because of the fact that the system would most likely return to the default peg setting of $1 and that this is a rare event. IT would be creating an opportunity out of the problem.

There’s also the 19% APR which is central to the system and on its own is massive and to a large extent offers a hedge against unpeg.

And for LUNA this means a net positive inflow of capital. It makes no difference whether UST is minted at a rate of $0.8 or $0.7 or $1 because it burns LUNA supply. And supply change vector is key for investors. Investors’ confidence is the core goal here and is what adds a disproportionate amount of elastic resources that can support the project.

LUNA would be capable to burn supply even when it’s in crisis mode and thus leverage on the potential trust of investors that are witnessing this.

Think of the unpeg event as a point where the two systems start to pull away from each other with UST hurting LUNA and in the end LUNA destroying UST. And the determinant for this is the level of collateralization.

Having this mechanism in place coupled with the other points would create immediate protection. Again the emphasis is on this happening extremely rarely, but it is still critical to have the logic bound into the protocol as that would give investors some peace of mind. We expect the unpeg to deviate with less significance because of this.

In fact, I think the May 11 drop, in this case, would not have exceeded $0.7

On May 11

k(LUNA) = $9.5B

k(UST)= $14B

The fair price of UST would be $0.67 probably for a brief moment of time. Markets would try to push prices higher, which means there would be a strong burn effect on LUNA. And UST would recover because of the recovery of the underlying asset.

This would also enable professional market makers to define the accurate mid-price to continue providing liquidity with little uncertainty.

Yes, it would be stressful but likely short-term and it can be communicated to affected people. Also if the Anchor measures were in place with lockup, there would be no chance for a panic extraction of so much capital at once which further exacerbated the problem.

The price of UST would start recovering and would likely strengthen its position in an effort to benefit from the inversion, which would be rare, but still a pre-planned event. It is quite possible for such crashes to actually turn into flash crashes as professional market makers would be most likely the ones to seize the opportunity.

8) Utilize all swap fees collected as a staking reward to the disaster fund providers and ensure the fund has a smooth transition to the new collaterized mechanism that will essentially do the same → buy back Luna, in case of future inversions.

Our team remains available for not only assisting but further providing evidence of our findings and also working with the team of Terra should they consider this to be a proposal of interest.